The Crude Chronicles - Episode 9

Trade Deal Delay Bearish for WTI

Benchmark WTI prices have been broadly lower over the week as concerns for the global economy have once again weighed on the outlook for oil demand.

The week commenced with a note of uncertainty over US-Sino trade relations. Late last week, On the back of two days of meetings in Washington, President Trump announced that a verbal deal had been reached (named “phase one”) which would form the first step towards ending the two -year long trade war which has ravaged the global economy. Trump told reporters that China had agreed to a massive new quota of US agricultural purchases in exchange for the US abandoning plans to increase tariffs on $250 billion of Chinese goods.

However, Chinese leaders were reportedly concerned over the details laid out in the deal and registered their reluctance to sign until the details had been ironed out. The market was spooked by this development, leading to a wave of risk aversion over the week which weighed on WTI prices.

News of China’s hesitation over signing the deal was followed swiftly by a warning from US Treasury Secretary Steve Mnuchin who said that if China did not sign a deal by December 15th, the US would continue with the next round of tariffs on $156 billion of Chinese goods planned for that date.

Currently, the US is pushing for the deal to be signed by the November APEC meeting in Chile, to be attended by both the president and Chinese premier Xi. Deputy level talks are scheduled for next week to keep things moving. However, if there is any further delay this is likely to drag oil down lower in the short term.

Oil prices also came under pressure this week from the latest IMF World Economic Outlook. The IMF now forecasts global growth to register a 3% reading by the year-end, marking a 0.2% downward revision from its last update in July. This would be the weakest global growth reading since 2008 and has raised further fears over the demand outlook for oil. Alongside its projection, the IMF warned over recessionary risks to the global economy noting that a reading of 2.5% or below would mean the global economy was in recession.

In its monthly forecast delivered this week, the EIA projects US crude output from seven major shale sites to mark an increase of 58-000 barrels per day over November to hit record highs of 8.971 million bpd. Of the seven sites noted, the Permian Basin of Texas and New Mexico is projected to mark a 63k barrel per day increase to 4.547 million bpd, marking a tenth consecutive increase. The IEA also forecasts US natural gas production to rise by 84 billion cubic feet per day over the month marking a 03bcfc increase on the last forecast made in October.

EIA Inventories Report Delayed

The EIA will release its latest US oil inventories report today ( a day behind schedule due to the Columbus day holiday) and is expected to register a 3million barrel increase, marking a further rise from last week’s 2.9 million barrel surplus. This would mark the fifth consecutive weekly increase in US crude stores and amidst the ongoing uncertainty over the demand outlook for oil, would be heavily bearish for WTI prices. Traders should also pay attention to crude production levels which could add to the downside for WTI prices if a further increase is seen from last week’s record highs.

Technical & Trade Views

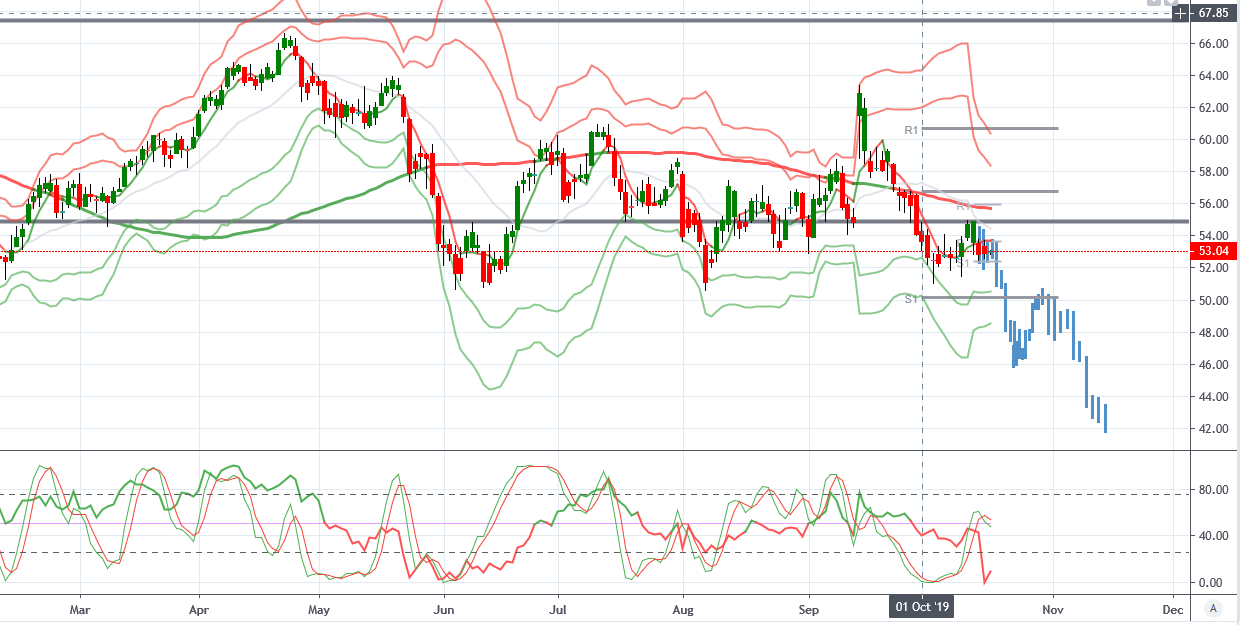

WTI Crude (Bearish, while $55 holds, targeting $45)

WTI From a technical and trade perspective. The retest of $55 has seen offers kicking in as expected with WTI reversing lower now. In line wth longer-term VWAP I will be looking for a break of the monthly S1 at $50 where we also have a few big previous swing lows. Once below here, any retest of the level should offer further short opportunities moving down towards $45.

Please note that this material is provided for informational purposes only and should not be considered as investment advice. The views discussed in the above article are those of our analysts and are not shared by Tickmill. Trading in the financial markets is very risky

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!